Breaking Down the Game Film: Three Clubs, One Season’s Lesson

Every coach knows that game film rarely lies. The camera captures not only the goals and the glory but also the hesitation in the midfield, the moments of fatigue, the clever adjustments, and the reckless errors. When I sat down to review the long arc of twenty years’ worth of investing, it felt exactly like that: studying the tape of three very different clubs, each with its own philosophy, its own tactics, and its own fortunes rising and falling with the seasons.

The first team, let’s call them Club A, reminds me of a relentless side built on stamina and structure. Their approach is not glamorous, and it certainly is not flashy. Rather, it is the kind of disciplined, high-press football that chokes the opposition, slowly and surely grinding them down. Month after month, year after year, Club A never abandoned the game plan. Contributions kept flowing like steady passes, each one unremarkable in isolation but devastating in accumulation, until the rhythm itself became impossible to disrupt.

Club B, on the other hand, struck me as a more conservative squad, content to hold its shape and wait for opportunities. They weren’t trying to dominate possession, nor were they particularly ambitious in attack. Instead, they sought to rely on dividends the way a pragmatic side leans on set pieces: the odd corner, a well-taken free kick, a tidy goal here or there. Their seasons rarely spiraled out of control, but neither did they electrify the pitch. Watching their film, you get the sense of a mid-table club — sturdy, respectable, but rarely lifting silverware.

Then came Club C, a side far less predictable. Their strategy was part dividend, part property play — the kind of hybrid approach that looks brilliant when the counterattack lands but leaves the back line dangerously exposed. Some years their surges were breathtaking, as if they were a cup team destined to shock the giants. Other years, they were caught flat, forced into painful retreats, scrambling to rebuild. By the end of 2022, they made a dramatic substitution, selling off the real estate leg of their formation and redeploying fully into equities. It was bold, it was risky, and it gave them moments of thrilling momentum. Yet, as any coach knows, such volatility comes at a cost: consistency.

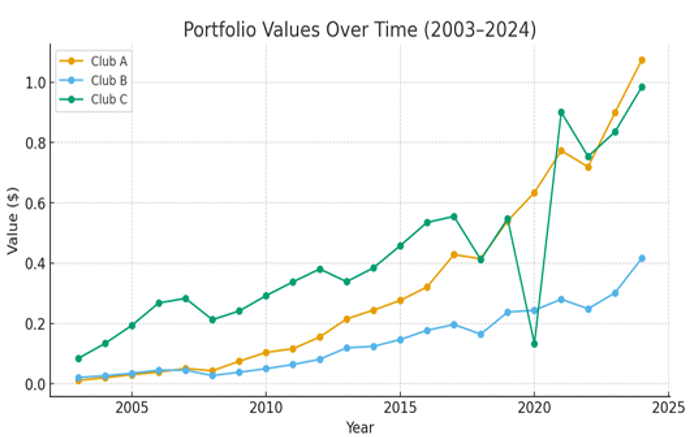

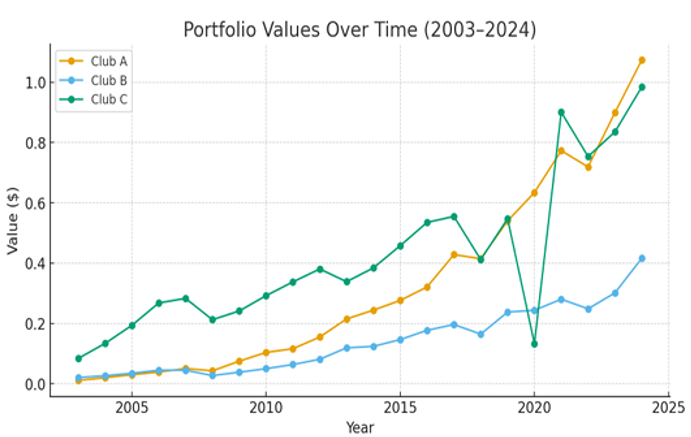

Portfolio Values Over Time

And so, if you track the tape across the years from 2003 to 2024, the story unfolds with unmistakable clarity:

Club A’s line on the graph arcs upward with remarkable steadiness, as though their press never tired, as though compounding itself was their star striker converting every half-chance.

Club B lags behind, their climb respectable but gradual, mirroring their measured, defensive posture.

Club C zigzags: moments of brilliance punctuated by stalls, a side that thrilled the crowd but tested the nerves of its supporters.

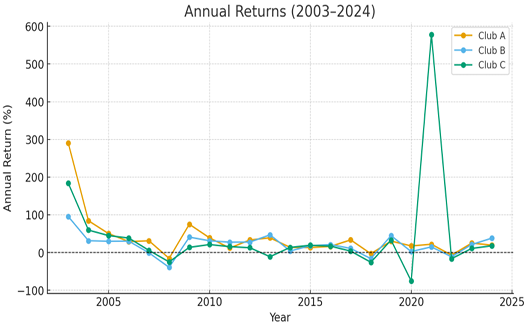

Annual Returns

When we switch angles and study the highlight reels — the season-by-season returns — we see the drama unfold even more vividly:

Club A’s performance has its bumps, but their line reflects a consistency that speaks to preparation and discipline. Club B is the definition of cautious play: fewer wild swings, but also fewer decisive victories. And Club C, well, their volatility is on full display. One year, they storm the pitch with spectacular gains; the next, they’re routed, conceding ground in humiliating fashion.

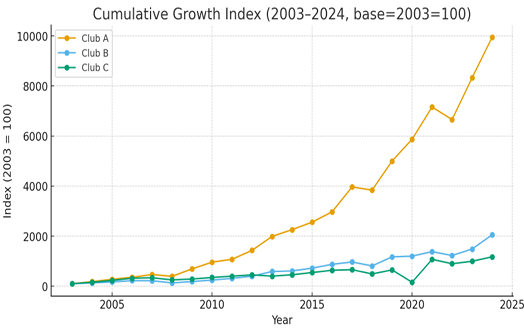

Cumulative Growth Index

Finally, when we turn to the cumulative standings — the equivalent of the league table over two decades — the result is undeniable:

Club A emerges as the clear champion. Their disciplined system, their refusal to abandon the high press, their commitment to contribution after contribution; it all compounded into dominance.

Club C, despite moments of brilliance, could not overcome the chaos of their own inconsistency.

Club B, steady but uninspired, held their place respectably but without ever threatening to climb to the very top.

The Reveal

Now here’s where the film reveals its final twist. These were not three different clubs at all. They were, in fact, three different accounts from my own career:

- Club A was my TSP (Thrift Savings Plan): the account I contributed to regularly, untouchable, the disciplined system that could not be interrupted.

- Club B was my Individual IRA: my conservative, dividend-focused account, slower and steadier, but never explosive.

- Club C was my Taxable Brokerage Account: the flexible one, sometimes raided for real estate opportunities, later sold and reinvested into the market.

And so the lesson, as clear as the final whistle, is this: in both soccer and investing, the team that plays with discipline, that refuses to deviate from its system, and that trusts in the slow build-up rather than chasing chaos, is the one that ends the season holding the trophy.

In my own life, that team was my TSP.

However, TSP wasn’t an option for me for the first 14 years of my military career. It was first offered to me in March 2002. By that time, I had accumulated a little over $10k in my Individual IRA account along with ~$15k in my Brokerage Account. So both accounts had a significant lead over TSP in the beginning years.

Let’s take a look at Chart 1 (Portfolio values Over Time).

The first 5 years TSP and my individual IRA accounts closely match each other. My individual IRA accounts were invested in Dividend paying stocks, while TSP was invested in low cost index funds. Starting in 2007, I began maxing out my TSP investments, which is why you start seeing the separation between the two funds in 2008. Notice my Brokerage Account was clearly the leader until 2017. In 2013, 2018 and 2020, I raided my Brokerage Account to buy real estate. At the end of 2021 I sold the real estate, and re-invested the proceeds back into my brokerage account. But even that one time gain, didn’t keep up with the momentum of my TSP account.

For those who work for the government and have access to the Thrift Savings Plan, this is a huge benefit. Take full advantage of it. If you have access to a similar 401k plan, also take advantage of it.

In my experience, nothing beats a High Savings Rate combined with investing it into a low-cost index fund. Just as with film, the chart doesn’t lie. A high savings rate, combined with a low-cost index fund consistently performs, especially when giving it a time horizon of a decade or more.

It’s this 20+ years of investment experience that yields the Simpli-FI.money approach:

- Spend less than you earn. Live intentionally, avoid lifestyle creep, and focus on what truly matters.

- Invest the rest. Put your savings into low-cost index funds, automate the process, and let compounding do the heavy lifting.

- Avoid debt. Don’t let credit cards, car loans, or oversized mortgages hold you back—choose wisely and live below your means.

- Give it time to grow. With patience and consistency, decades of compounding will set you free.

If one maintains a high savings rate between 20-30% (or more) while avoiding the temptation of debt, time and compounding will take care of itself. Once you’ve set your savings rate, you don’t have to worry about the individual spending decisions so much. You’ve already set yourself on a course that will lead you to victory. You can free your mind on the other things that matter more.

Want to see your timeline? Use Coach Holdren’s Simple Economic Model Calculator and plug in your numbers. Link: S.E.M. Calculator – Simpli-FI.money