I’m Coach Holdren, a high school soccer coach, retired military officer, and a 60-year-old who’s made more money mistakes than I care to admit. I also hold master’s degrees in Systems Engineering, Economics, and Strategic Studies. You’d think those degrees would have made me immune to financial blunders. Nope. I chased “hot” stocks, tried to time the market, and let lifestyle creep nibble away raises. None of that built freedom.

What did? Habits. The same lesson I hammer into my players; small, repeatable actions win seasons; is the lesson that finally fixed my finances. Money isn’t a puzzle for geniuses. Money is simple when your habits are simple.

For more than 20 years I saved between 20–30% of my income, automatically, into low-cost index funds. I avoided new debt, kept expenses below my income, and let time do the heavy lifting. That’s it. No lottery ticket, no perfect stock pick, no market-timing magic. Just compounding, which isn’t luck; it’s a law of nature. Gravity pulls a ball to the ground every time; compounding pulls your wealth upward every year you stay consistent.

The Simpli-FI Playbook I Follow

- Spend less than you earn. Live intentionally and ignore the herd.

- Invest the rest, automatically, into broad, low-cost index funds.

- Avoid debt. Don’t let credit cards, oversized cars, or bloated mortgages run your life.

- Give it time. Decades, not days. Let compounding work.

Those savings flow into what I call the Freedom Fund—the engine that covers expenses when work becomes optional. To keep choices clear, I use two simple definitions:

- Financial Freedom: Investment income (a conservative 4% withdrawal from the Freedom Fund) covers expenses.

- Financial Independence: That same 4% covers your entire income; work is purely optional.

If you remember nothing else, remember this: assets put money in your pocket; liabilities take it out. Buy assets first. Later, let your assets buy the “nice-to-haves.”

What My Models Show (and Why They Built My Confidence)

I like numbers. They keep me honest when emotions get loud. Here are the three models I use with families and players—built on simple assumptions: income and expenses grow 3%/yr (inflation rate), your gap is income − expenses, your portfolio compounds at a rate that doubles about every 10 years (~7.18%), and your “investment income” is a 4% withdrawal of that growing balance.

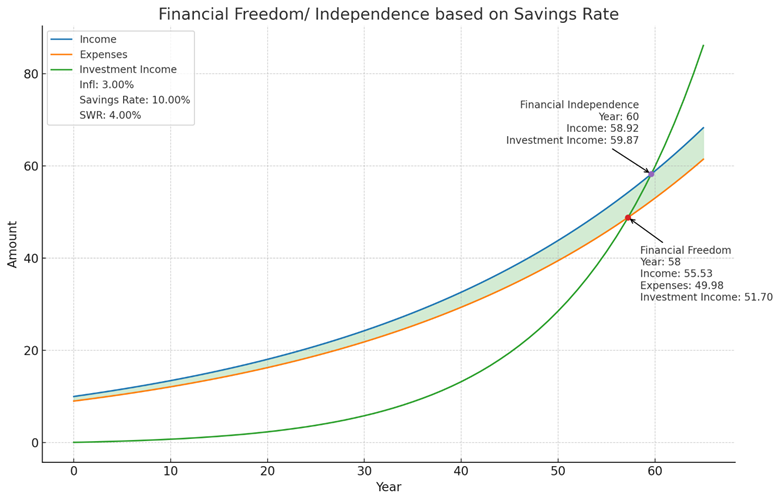

1) When I saved ~10% (early years)

I tried this first. It worked, but very slowly. Freedom didn’t show up for a long time.

- Financial Freedom: ~Year 58 (investment income ≈ 51.70)

- Financial Independence: ~Year 60 (investment income ≈ 59.87)

Ten percent is better than nothing, but it relies on a lot of time. If you’re 20 and patient, great. If you’re 40 or 50 and want options sooner, turn the dial.

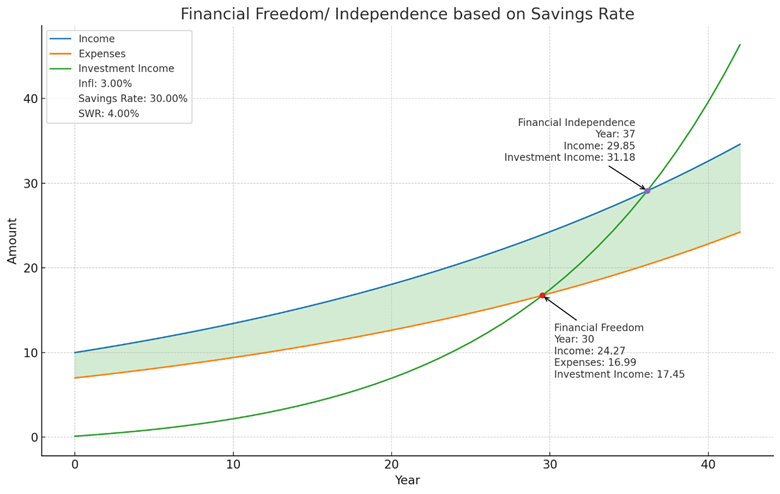

2) When I committed to 20–30% (what I did for 20+ years)

This is where everything changed for me. I didn’t get rich overnight; I just stopped fighting math and started using it.

- Financial Freedom: ~Year 30 (≈ 17.45)

- Financial Independence: ~Year 37 (≈ 31.18)

Saving 20–30% compresses decades into years. This is the lane where ordinary people, coaches, teachers, enlisted folks, small-business owners—actually reach freedom.

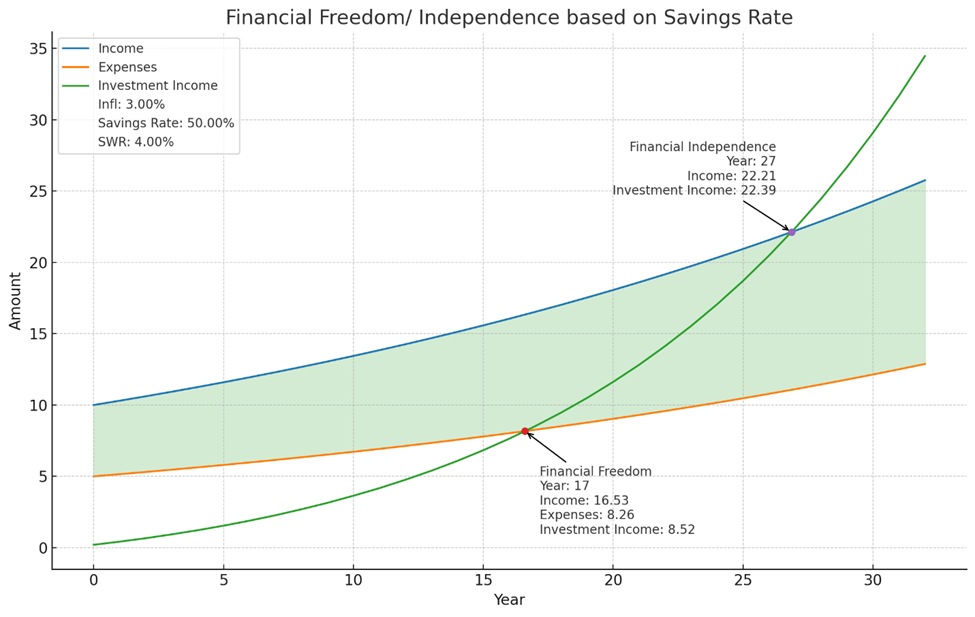

3) When life allowed 50% (short sprints of aggressive saving)

There were seasons, deployment, bonuses, kids out of daycare, when we could push to 50%. That’s like putting a turbo on compounding.

- Financial Freedom: ~Year 17 (≈ 8.52)

- Financial Independence: ~Year 27 (≈ 22.39)

Not everyone can live on half their income, and you don’t have to do it forever. But even a few years at 40–50% can radically pull your timeline forward.

What I’d Tell My 30-Year-Old Self

Stop trying to be clever. Be consistent. Automate transfers the day your paycheck lands. Keep your fixed costs low so raises actually boost your savings rate. When markets wobble (they will), keep contributing. Let the law of compounding do what it always does, quietly, reliably, like gravity.

And if you’ve made mistakes? Same. Me too. Start today. The best time to plant the tree was years ago; the second-best time is now. You don’t need perfection—you need progress that repeats.

Your Checklist (print this)

- Spend less than you earn.

- Invest the rest.

- Avoid debt.

- Let compounding do the rest.

- Know the difference between assets (put money in your pocket) and liabilities (takes money out).

- Buy assets first; use their income to buy what you need.

- Your savings rate sets your timeline.

Now It’s your turn. Act in your own best interest by “paying yourself first” (not last), and keep going. The math will meet you halfway.

We created a Financial Freedom/Independence Calculator (Coach Holdren’s Simple Economic Model (SEM)) where you can test out your own assumptions. You will find the calculator under the “S.E.M. Calculator” tab or click this Link: S.E.M. Calculator – Simpli-FI.money.